Payroll taxes in Mexico are one of the hardest things to understand when establishing your business in Mexico. Whether you are starting a Mexican maquiladora through the IMMEX program or a small software development firm, this article will be helpful.

Although there is one employer payroll tax, this article discusses all the payroll taxes, including social security and withholding taxes. All of these taxes are set out in Mexican labor laws.

IMPORTANT: This article has been updated according to the latest state-level payroll tax changes.

We can divide payroll taxes in Mexico into two categories: taxes the employee pays and those the company pays. Our article, Mexican Withholding Tax: How Much To Retain, discusses the portion the employee pays and the portion the company withholds. Similarly, in our article Social Security In Mexico: The Whole Picture, we take an in-depth look at how social security works and all of the specific concepts of the contributions.

In this article, we discuss payroll taxes in detail. Hence, we explain the burden to the company and how much the employee truly gets into his/her pocket.

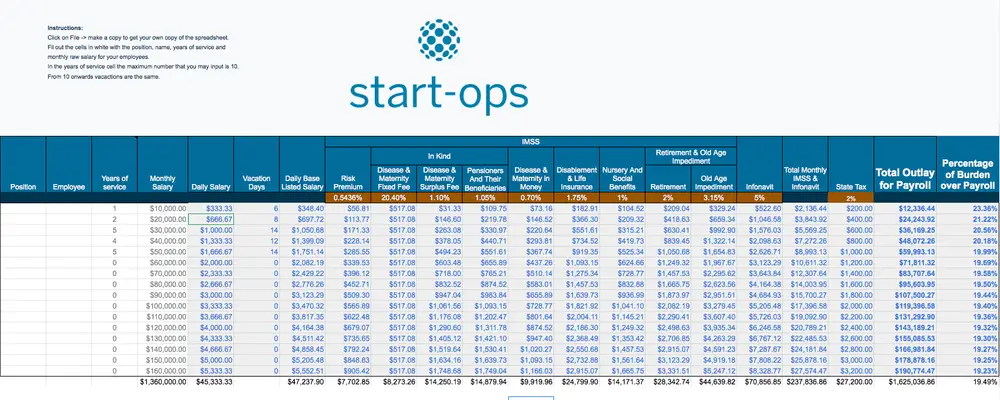

To simplify things, we created a tool called Mexico’s Payroll Taxes Calculator. Indeed, we advise you to read on to understand these concepts and what is happening. However, this tool lets you quickly see how much it will cost to have employees in Mexico.

If you wish to understand all taxes in Mexico, we recommend you read our Mexican taxes guide for foreigners.

So, let’s get to it.

To easily navigate this guide you can use the following table of content:

Employer Payroll Tax in Mexico: A State-Level Tax

Firstly, Mexico has federal-level taxes and state-level taxes. The federal-level taxes are the same all over Mexico, and the state-level taxes, as you can probably guess, vary according to the state where the business is located.

Employer payroll tax in Mexico is a state-level tax, and it’s pretty straightforward. It is charged as a percentage of the entire payroll, and is the employer’s duty to pay it. The rate ranges between 1% and 3% of salaries, depending on the state in your business is located.

Mexican Employer Payroll Tax Rate By State

So, how does this work?

Well, once your company hires employees in Mexico, Start-Ops will assist you with the accounting and tax compliance. Although we offer a treasury service, it’s not uncommon for companies to handle their bank accounts through their teams abroad. So, in this case, we would send you a tax payment sheet once per month that looks something like this.

This payroll tax sheet is from Mexico city, which is considered a state on its own. Each state has its own format but they are more or less the same.

Mexican Withholding Tax

As we said in this article, we cover all of the taxes involved in payroll in Mexico. This section discusses the income tax employees pay to the Mexican government. However, it is the company’s responsibility to withhold it and pass it over to the SAT (Mexican tax authorities).

If you wish to have an in-depth understanding of how this works, you can check out this article on Mexican Withholding Tax; here, we will provide a summary.

Firstly, as stated before, this is the income tax that employees pay as individuals. First, we need to know how much income tax individuals are charged in Mexico.

The following table summarizes it.

Step-by-step calculation:

- Check the income level where the salary falls between the lower and higher limits.

- Subtract the lower limit from the salary. The difference obtained is called a surplus.

- Apply the tax rate for the salary’s income level to the surplus.

- Add the fixed fee, based on income level, to the surplus taxes.

Don’t worry, we do the complete step-by-step calculation in an example ahead in this article.

Employment Subsidy

Tax authorities benefit employees with low-income levels, for example, workers making the minimum wage in Mexico by subsidizing their income tax. So, in these cases, companies need to withhold less.

The following table summarizes the subsidy categories.

Step-by-step calculation:

- Check the level of income where the salary ranks between the lower limit and higher limit.

- Discount the subsidy from the employees income tax to pay.

Social Security: A Part of Payroll Taxes in Mexico

Social Security is part of Mexican payroll taxes. To know more about this subject, read our in-depth article on social security in Mexico. However, we will provide a basic summary in this article.

Let us start with a bit of background.

The Mexican Social Security Institute, or IMSS (Instituto Mexicano del Seguro Social in Spanish), is responsible for social security in Mexico. Its mission is to provide medical attention and social security to all Mexican workers or employees. Therefore, every Mexican employee in the private sector has the right to social security benefits.

Both workers and companies need to contribute to social security. However, the company is responsible for withholding this contribution and paying it to the IMSS. At first sight, this may seem expensive, but it also has benefits. For example, when a working mother gets maternity leave in Mexico, the institute covers 100% of her salary for 12 weeks.

INFONAVIT: Social Housing In Mexico

Employers need to contribute to workers’ social housing as part of social security. Although a different institute manages social housing called the National Housing Fund Institute (INFONAVIT, for its name in Spanish), it is part of social security and is closely related to the IMSS.

Employer-Employee Fees

The total amount paid to the IMSS is called Employee—Employer Fees or Cuotas Obrero—Patronales. The company (employer) is responsible for paying it. However, the employee contributes a proportion of the payment. The idea is that he is contributing a small proportion of his salary toward his social security payments. So, to correctly calculate payroll taxes in Mexico, we need to understand the deductions that go to the IMSS and INFONAVIT.

Most of the concepts are calculated as a proportion of the Base Listed Salary, which is a concept we will see further ahead in this article.

Going from top to bottom, the first thing we need to find out is the Work Risk Premium.

So let’s take a look at this concept.

Work Risk Insurance

According to the type of risk that workers undertake in their jobs, the IMSS has categorized five different risk levels going from less dangerous to more. Obviously, level I is assigned to administrative work in an office environment, and level V to the riskiest job you can imagine. The following tables show the levels of risk with their related risk premium.

How To Calculate Payroll Taxes In Mexico

In this section, we will show you, step by step, how to calculate payroll taxes in Mexico. We strongly recommend that you download our Mexico’s Payroll Tax Calculator and use these instructions to understand what’s going on. It will make things a lot easier for you.

First, to calculate social security, we need to obtain the Base Listed Salary (BLS).

Calculating Social Security in Mexico

Base Listed Salary

According to Article 27 of Mexico’s Social Security Law, benefits are calculated based on the employees’ Base Listed Salary. The term in Spanish is Salario Base de Cotización (SBC). The main difference from the regular salary is that it includes bonuses, commissions, etc.

The BLS is integrated with all payments made in cash regarding:

- Daily Payment

- Gratifications

- Premiums

- Commissions

- Payments in Kind

- Any Other Retribution

For practical purposes, we will assume an employee who receives only his regular salary.

To obtain the BLS, you must integrate all the mandatory employee benefits, i.e., vacations, vacation premium, and Aguinaldo (Christmas bonus), into the worker’s salary.

If you want to know more about these concepts, we recommend reading our Employee Benefits in Mexico article.

Here’s a quick summary.

- Vacations. If an employee has worked for the company for over a year, he is entitled to paid vacation each year. This period starts at 12 days, and two days are added for each year of continuous employment in the company until the fifth year, when 20 days are reached. After that, it is increased by two days every four years.

- Vacation Premium. Vacation days are paid at an extra 25% premium on top of the regular salary.

- Christmas Bonus. If an employee has worked for the company for over a year, he is entitled to a Christmas bonus of 15 days’ salary.

The first step is to calculate the employee’s regular daily salary. Let’s see an example. Let’s think about Raul, an excellent employee who has worked for 2.5 years and earns MXN 10,000 per month.

Since Raul has continuously worked for your company for one year, he is entitled to 12 days of vacation.

So, we calculate this by first obtaining a factor.

Let’s see how it’s done.

- Christmas Bonus: 15 days.

- Vacations 12 days.

- Vacation Premium of 3 days (12 days * 25%).

Then we multiply Raul’s daily salary by the integration factor to obtain his daily & monthly BLS.

We know that Raul’s daily BLS is $360.73, and all social security contributions will be applied to that amount. The next step is to find out what’s the risk premium.

Calculating Risk Premium

Since Raul is an administrative worker and works at an office, the risk premium would be Class I, with a premium of 0.54355%.

Secondly, we need to calculate the surplus fee for the In-Kind part of Disease and Maternity Insurance. The surplus is the difference between the worker’s monthly BLS and three times monthly UMA.

Thirdly, we need to calculate the employer’s Advanced Age Severance Fee.

Calculating Employer’s Advanced Age Severance Fee

In December 2022, there was an amendment to the Article 168 of the Socia Security Law. This benefit is calculated from January 1st, 2023, according to the following table.

Since we know Raul’s daily BLS is 360.73, it ranks in category six. Therefore, we know the Advanced Age Severance fee is 9.57%.

Now we have everything we need to calculate social security for our employee, Raul.

- Monthly BLS = $10,684.80

- Risk Premium = 0.54355%

- Disease & Maternity Insurance Surplus = $1,369.82

- Advanced Age Severance Rate: 9.57%

The rest is calculated directly from the BLS.

IMSS Calculation for a $10,000 Salary

- Company’s Contribution = $2,997.32

- Employee’s Contribution = $262.46

Now, let’s move on to calculate the employer’s payroll tax in Mexico.

Calculating Employer Payroll Taxes in Mexico

This one is quite easy. Firstly we need to find the state where our company is located on the table. Remember that this is a state-level tax. Let’s assume that our company is based in Jalisco, so our employer payroll tax would be 2.5%.

This 2.5% is applied directly to the regular salary, which, continuing with Raul’s example, is $10,000. And this part is fully paid by the company.

- Company’s Payroll Taxes = $250

Calculating Withholding Tax in Mexico

So by now, we have already calculated social security and employer payroll taxes in Mexico. All that’s left is to calculate the amount of income tax we need to withhold for Raul.

Firstly, we need to find his level of income in the Income Tax For Individuals Table.

Step-by-step calculation:

- Check the level of income where the salary ranks between the lower limit and the higher limit.

- Subtract the lower limit from the salary. The difference obtained as a result is called a surplus.

- Apply the tax rate of the salary’s level of income to the surplus.

- Add the fixed fee according to the level of income to the surplus taxes.

Let’s do it step by step in the following table.

- Employee Income Tax: $606.57

So we know that we need to withhold $606.57 from Raul’s paycheck and pass it over to the tax authorities. Since he makes more than $7,382.34, he doesn’t get any subsidy.

Now, let’s summarize all of the payroll taxes in Mexico for Raul’s $10,000 salary.

Payroll Taxes In Mexico For A $10,000 Salary

Conclusion

Payroll taxes in Mexico are complicated but it isn’t something impossible to understand. You just need to know the underlying concepts and the rates that are charged. At Start-Ops we help you by taking care of all of the administrative hassle implied in opening a nearshore office. We are experts at providing all-inclusive soft-landing solutions. For everything your company needs to establish in Mexico, you can rely on us.

If your company is thinking about exploring nearshore options, get in touch with us. We can develop a business plan that takes into account all of the costs involved in moving a part of your business to Mexico.

One Response