Copyright © 2023 Start-Ops Mexico All rights reserved.

The reproduction and/or distribution of this document is expressly prohibited without prior written permission of the author.

You may not copy, reproduce, distribute, publish, display, perform, modify, transmit, nor may you distribute any part of this content over any network, including a local area network, sell or offer it for sale, or use such content to construct any kind of database.

Disclaimer

Legal texts and legal practice require close examination of terms and words and every sentence & paragraph can take very different meanings depending on how these are being interpreted.

This document is an AI assisted translation of the original in Spanish and it should be used for information

purposes only. The author of this document has made reasonable efforts to provide an accurate translation, however, in case of a discrepancy, the Spanish original will prevail before a court of law.

MEXICAN INCOME TAX LAW IN ENGLISH

New Law published in the Diario Oficial de la Federación on December 11, 2013.

CURRENT TEXT

Last amendment published DOF 01-04-2024

TITLE I

GENERAL PROVISIONS

Article 1. Individuals and corporations are obligated to pay income tax in the following cases:

I. Residents in Mexico, with respect to all their income, regardless of the location of the source of wealth from which it derives.

II. Residents abroad who have a permanent establishment in the country, with respect to the income attributable to such permanent establishment.

III. Residents abroad, with respect to income from sources of wealth located in national territory, when they do not have a permanent establishment in the country, or when having one, such income is not attributable to it.

For the purposes of this Law, a permanent establishment is considered to be any place of business in which business activities are carried out, partially or totally, or in which independent personal services are rendered. It shall be understood as permanent establishment, among others, branches, agencies, offices, factories, workshops, facilities, mines, quarries or any place of exploration, extraction or exploitation of natural resources.

Notwithstanding the provisions of the preceding paragraph, when a resident abroad acts in the country through an individual or legal entity, other than an independent agent, the resident abroad will be deemed to have a permanent establishment in the country, in connection with all the activities that such individual or legal entity performs for the resident abroad, even if it does not have a place of business in the country, if such person habitually concludes contracts or habitually performs the principal role that leads to the conclusion of contracts entered into by the resident abroad and the latter:

I. They are entered into in the name or on behalf of the same;

II. They provide for the alienation of the property rights, or the granting of the temporary use or enjoyment of an asset owned by the resident abroad or over which he has the right of temporary use or enjoyment, or

III. Oblige the resident abroad to provide a service.

Paragraph with reformed fractions DOF 09-12-2019

For purposes of the preceding paragraph, it will not be considered that there is a permanent establishment in Mexican territory when the activities carried out by such individuals or legal entities are those mentioned in Article 3 of this Law.

Paragraph added DOF 09-12-2019

In the event that a resident abroad performs business activities in the country through a trust, the place where the trustee performs such activities and complies on behalf of the resident abroad with the tax obligations derived from such activities will be considered as the place of business of such resident.

A permanent establishment of an insurance company resident abroad shall be deemed to exist when it receives income from the collection of premiums within the national territory or grants insurance against risks located therein, through a person other than an independent agent, except in the case of reinsurance.

Likewise, a resident abroad will be considered to have a permanent establishment in the country, when acting in the national territory through an individual or legal entity that is an independent agent, if the latter is not acting in the ordinary course of its business. For these purposes, it is considered that an independent agent is not acting in the ordinary course of business, among others, when it is located in any of the following cases:

Amended paragraph DOF 09-12-2019

I.It has stocks of goods or merchandise, with which it makes deliveries on behalf of the resident abroad.

II. Assume risks of the resident abroad.

III. Act subject to detailed instructions or to the general control of the resident abroad.

IV. Exercises activities that economically correspond to the resident abroad and not to his own activities.

V. Receive their remuneration regardless of the results of their activities.

VI. Performs transactions with the foreign resident using prices or amounts of consideration different from those that would have been used by unrelated parties in comparable transactions.

It is presumed that an individual or legal entity is not an independent agent when it acts exclusively or almost exclusively on behalf of foreign residents who are its related parties.

Paragraph added DOF 09-12-2019

In the case of construction, demolition, installation, maintenance or assembly services in real estate, or for projection, inspection or supervision activities related thereto, it will be considered that there is a permanent establishment only when such services have a duration of more than 183 calendar days, consecutive or not, in a twelve-month period.

For the purposes of the preceding paragraph, when the resident abroad subcontracts with other companies the services related to construction of works, demolition, installations, maintenance or assemblies in real estate, or for projection, inspection or supervision activities related to them, the days used by the subcontractors in the development of these activities will be added, if applicable, for the computation of the aforementioned term.

Income attributable to a permanent establishment in the country will be considered to be income derived from the business activity carried out or income from fees and, in general, from the rendering of an independent personal service, as well as income derived from the sale of merchandise or real estate in Mexican territory, carried out by the head office of the person, by another establishment of the person or directly by the resident abroad, as the case may be. Tax must be paid on such income under the terms of Titles II or IV of this Law, as applicable.

Income obtained by the head office of the company or any of its establishments abroad is also considered to be income attributable to a permanent establishment in the country, in the proportion in which said permanent establishment has participated in the expenses incurred to obtain such income.

A place of business whose sole purpose is to carry out activities of a preparatory or auxiliary nature with respect to the business activity of the resident abroad shall not be deemed to constitute a permanent establishment. It is considered that a permanent establishment is not constituted when the following activities are carried out, provided that they are of a preparatory or auxiliary nature:

Amended paragraph DOF 09-12-2019

I. The use or maintenance of facilities for the sole purpose of storing or exhibiting goods or merchandise belonging to the resident abroad.

II. The preservation of stocks of goods or merchandise belonging to the resident abroad for the sole purpose of storing or exhibiting such goods or merchandise or having them processed by another person.

III. The use of a place of business for the sole purpose of purchasing goods or merchandise for the resident abroad.

IV. The use of a place of business for the sole purpose of carrying out propaganda activities, providing information, scientific research, preparing for the placement of loans, or other similar activities.

Reformed fraction DOF 09-12-2019

V. The fiscal deposit of goods or merchandise of a resident abroad in a general warehouse nor the delivery of such goods or merchandise for importation into the country.

The preceding paragraph will not be applicable when the resident abroad performs functions in one or more places of business in Mexican territory that are complementary as part of a cohesive business operation, to those performed by a permanent establishment in Mexican territory, or to those performed in one or more places of business in Mexican territory by a related party that is a resident in Mexico or a resident abroad with a permanent establishment in Mexico. The preceding paragraph will also not be applicable when the resident abroad or a related party has in Mexican territory a place of business where complementary functions that are part of a cohesive business operation are carried out, but whose combination of activities results in not having a preparatory or auxiliary nature.

Paragraph added DOF 09-12-2019

The provisions of this article shall also apply in the case of activities carried out through a natural or legal person, other than an independent agent.

Paragraph added DOF 09-12-2019

The benefits of the treaties to avoid double taxation shall only be applicable to taxpayers that prove they are residents of the country in question and comply with the provisions of the treaty itself and the other procedural provisions contained in this Law, including the obligation to submit the information on their tax situation under the terms of Article 32-H of the Federal Fiscal Code or to submit the financial statement report when they are obligated to do so or have exercised the option referred to in Article 32-A of said Code, and to designate a legal representative.

Amended paragraph DOF 12-11-2021

In addition to the provisions of the preceding paragraph, in the case of transactions between related parties, the tax authorities may request the taxpayer resident abroad to prove the existence of legal double taxation by means of a declaration under oath signed by its legal representative, in which he expressly states that the income subject to taxation in Mexico and with respect to which the benefits of the treaty to avoid double taxation are intended to be applied, is also taxed in his country of residence, for which he must indicate the applicable legal provisions, as well as such documentation that the taxpayer considers necessary for such purposes.

In those cases in which the treaties to avoid double taxation establish withholding rates lower than those indicated in this Law, the rates established in said treaties may be applied directly by the withholder; in the event that the withholder applies rates higher than those indicated in the treaties, the resident abroad will have the right to request a refund for the corresponding difference.

The certificates issued by foreign authorities to prove residence will be effective without the need for legalization and it will only be necessary to show an authorized translation when required by the tax authorities.

Article 4-A. For purposes of this Law, foreign tax transparent entities and foreign legal entities, regardless of whether all or part of their members, partners, shareholders or beneficiaries accrue income in their country or jurisdiction of residence, will be taxed as legal entities and will be obligated to pay income tax in accordance with Title II, III, V or VI of this Law, if applicable. For purposes of the foregoing, when they comply with the provisions of Section II of Article 9 of the Federal Tax Code, they will be considered residents of Mexico.

Foreign entities are considered foreign entities, corporations and other entities created or incorporated under foreign law, provided that they have their own legal personality, as well as legal entities incorporated under Mexican law that are residents abroad, and trusts, associations, investment funds and any other similar legal entity under foreign law are considered foreign legal entities, provided that they do not have their own legal personality.

Foreign entities and foreign legal entities are considered fiscally transparent when they are not tax residents for income tax purposes in the country or jurisdiction where they are incorporated or where they have their principal place of business or effective management, and their income is attributed to their members, partners, shareholders or beneficiaries. When they are considered tax residents in Mexico, they will cease to be considered transparent for purposes of this Law.

The provisions of this article shall not apply to treaties for the avoidance of double taxation, in which case, the provisions contained therein shall be applicable.

Article added DOF 09-12-2019

Article 4-B. Residents in Mexico and residents abroad with a permanent establishment in the country for the income attributable to the same, are obligated to pay the tax in accordance with this Law, for the income they obtain through fiscally transparent foreign entities in the proportion that corresponds to them due to their participation in them. In cases where the foreign entity is partially transparent, taxpayers will only accrue the income attributed to them. In order to determine the amount of the income indicated in this paragraph, the calendar year taxable income of the foreign entity calculated under the terms of Title II of this Law will be considered.

Residents in Mexico and residents abroad with a permanent establishment in the country for the income attributable to the same, are also obligated to pay the tax in accordance with this Law, for the income obtained through foreign legal entities in the proportion that corresponds to them, regardless of their tax treatment abroad. In the event that the foreign legal entities are fiscally transparent, the income will be accumulated under the terms of the Title of this Law that corresponds to the taxpayer and will be taxable in the same calendar year in which they are generated. In these cases, taxpayers may deduct the expenses and investments made by the legal entity provided that they are deductible in accordance with the Title of this Law that corresponds to them, as long as it is done in the same proportion as the income accrued and in compliance with the general rules issued by the Tax Administration Service.

In the event that foreign legal entities are considered tax residents in a country or jurisdiction abroad or in Mexico, the amount of income will be the taxable income of the calendar year of such legal entity calculated under the terms of Title II of this Law and must be accrued by the taxpayer as of December 31 of the calendar year in which they were generated.

The provisions of this article will only be applicable when the Mexican resident has a direct participation in the fiscally transparent foreign entity or foreign legal entity, or when they have an indirect participation involving other fiscally transparent foreign entities or foreign legal entities. In the event that their indirect participation involves at least one foreign entity that is not fiscally transparent, the income obtained through the fiscally transparent foreign entity or foreign legal entity in which the foreign entity that is not fiscally transparent has a participation will be subject to the provisions of Chapter I of Title VI of this Law, if applicable.

Income obtained in accordance with this article will be considered generated directly by the taxpayer. Taxes paid by or through transparent foreign entities or foreign legal entities referred to in this article, shall be considered paid directly by the taxpayer, in the same proportion in which they have accrued the income of such entity or entity.

If the income of the foreign entity or foreign legal entity is subject to a tax established in this Law and such tax has been effectively paid, the same may be credited by the taxpayer under the terms of Article 5 of this Law and other applicable tax provisions. In these cases, the same will be creditable in its totality considering the same proportion in which the income of such entity or legal entity has been accrued.

The taxpayers mentioned in this article must keep an account for each of the foreign tax transparent entities and foreign legal entities under the same terms of article 177 of this Law, in order not to duplicate the accrual of income when such entity effectively distributes a dividend or profit, or when the legal entity delivers such income or makes it available to the taxpayer.

Foreign entities are considered to be partially transparent when the foreign tax law in question attributes a portion of their income to their partners or shareholders, while the remaining portion is attributed to such entity.

The provisions of the preceding paragraphs will be applicable even when the foreign fiscally transparent entity or foreign legal entity does not distribute or deliver the income regulated by this article. In order to determine the proportion of the income corresponding to the taxpayers on the foreign fiscally transparent entities and foreign legal entities, the provisions of the fourth and fifth paragraphs of article 177 of this Law will be considered, regardless of whether the persons obligated in accordance with this article do not have control over such entities or legal entities.

Additionally, the accounting records of the foreign fiscally transparent entity or foreign legal entity, or the documentation that allows verifying its expenses and investments, must be available to the tax authorities. In case of failure to comply with this obligation, the deduction of expenses and investments made by such entity or legal entity will not be allowed.

Article added DOF 09-12-2019

Article 5. Residents in Mexico may credit, against the tax they are required to pay pursuant to this Law, the income tax they have paid abroad on income from a source located abroad, provided that it is income for which they are required to pay the tax under the terms of this Law. The crediting referred to in this paragraph will only proceed provided that the accrued income, received or accrued, includes the income tax paid abroad.

In the case of income from dividends or profits distributed by companies resident abroad to legal entities resident in Mexico, the proportional amount of income tax paid by such companies that corresponds to the dividend or profit received by the resident in Mexico may also be credited. Whoever makes the crediting referred to in this paragraph will consider as accumulated income, in addition to the dividend or profit received, without reducing the withholding or payment of income tax that may have been made for its distribution, the proportional amount of the corporate income tax paid by the company, corresponding to the dividend or profit received by the resident in Mexico, even when the crediting of the proportional amount of the tax is limited in terms of the seventh paragraph of this article. The crediting referred to in this paragraph will only proceed when the Mexican resident entity owns at least ten percent of the capital stock of the foreign resident company, at least during the six months prior to the date on which the dividend or profit in question is paid.

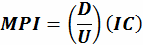

For the purposes of the preceding paragraph, the proportional amount of the income tax paid abroad by the company resident in another country corresponding to the dividend or profit received by the legal entity resident in Mexico will be obtained by applying the following formula:

Where:

MPI: Proportional amount of income tax paid abroad by the foreign resident company in the first corporate level that distributes dividends or profits directly to the legal entity resident in Mexico

D: Dividend or profit distributed by the foreign resident company to the legal entity resident in Mexico without deducting the income tax withholding or payment, if any, that may have been made for its distribution

U: Profit that served as the basis for distributing dividends, after payment of income tax at the first corporate level, obtained by the foreign resident company that distributes dividends to the legal entity resident in Mexico

IC: Corporate income tax paid abroad by the foreign resident company that distributed dividends to the Mexican resident entity

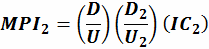

In addition to the provisions of the preceding paragraphs, the proportional amount of the income tax paid by the foreign resident company that distributes dividends to another foreign resident company may be credited if the latter, in turn, distributes such dividends to the Mexican resident entity. Whoever makes the crediting in accordance with this paragraph, must consider as cumulative income, in addition to the dividend or profit received directly by the Mexican resident entity, without reducing the income tax withholding or payment that may have been made for its distribution, the proportional amount of the corporate income tax that corresponds to the dividend or profit received indirectly for which the crediting is to be made, even when the crediting of the proportional amount of the tax is limited in terms of the seventh paragraph of this article. This proportional amount of income tax paid at a second corporate level will be determined in accordance with the following formula:

Where:

MPI2: Proportional amount of income tax paid abroad by the foreign resident company in the second corporate level, which distributes dividends or profits to the other foreign company in the first corporate level, which in turn distributes dividends or profits to the Mexican resident entity

D: Dividend or profit distributed by the foreign resident company to the legal entity resident in Mexico without deducting the income tax withholding or payment, if any, that may have been made for its distribution

U: Profit that served as the basis for distributing dividends, after payment of income tax at the first corporate level, obtained by the foreign resident company that distributes dividends to the legal entity resident in Mexico

D2: Dividend or profit distributed by the foreign resident company to the foreign resident company that distributes dividends to the Mexican resident entity, without deducting the withholding or payment of income tax that, if applicable, has been made for the first distribution

U2: Profit that served as the basis for distributing dividends after payment of income tax at the second corporate level, obtained by the foreign resident company that distributes dividends to the other foreign resident company that distributes dividends to the Mexican resident entity

IC2: Corporate income tax paid abroad by the foreign resident company that distributed dividends to the other foreign resident company that distributes dividends to the Mexican resident entity

The crediting referred to in the preceding paragraph will only proceed provided that the foreign resident company that has paid the income tax to be credited is in a second corporate level. In order to make such credit, the Mexican resident entity must have a direct participation of at least ten percent in the capital stock of the foreign resident company that distributes dividends to it. The latter company must own at least ten percent of the capital stock of the foreign resident company in which the Mexican resident has an indirect participation, and the latter participation must be at least five percent of its capital stock. The percentages of shareholding indicated in this paragraph must have been maintained for at least six months prior to the date on which the dividend or profit in question is paid. In addition, in order to make the credit referred to in the preceding paragraph, the foreign resident company in which the Mexican resident entity has an indirect participation must be a resident of a country with which Mexico has a comprehensive information exchange agreement.

In the case of corporations, the amount of the creditable tax referred to in the first paragraph of this article will not exceed the amount resulting from applying the rate referred to in article 9 of this Law to the taxable income resulting in accordance with the applicable provisions of this Law for income received in the year from a source of wealth located abroad. For these purposes, deductions that are attributable exclusively to income from a source of wealth located abroad will be considered at one hundred percent; deductions that are attributable exclusively to income from a source of wealth located in Mexican territory must not be considered, and deductions that are attributable partially to income from a source of wealth in Mexican territory and partially to income from a source of wealth abroad will be considered in the same proportion that the income from the foreign country in question represents with respect to the total income of the taxpayer for the year. The calculation of the crediting limit referred to in this paragraph will be made for each country or territory in question.

Additionally, in the case of corporations, the sum of the proportional amounts of taxes paid abroad that are entitled to be credited in accordance with the second and fourth paragraphs of this article, shall not exceed the crediting limit. The crediting limit will be determined by applying the following formula:

Where:

LA: Creditfor corporate income taxes paid abroad at the first and second corporate levels

D: Dividend or profit distributed by the foreign resident company to the legal entity resident in Mexico without deducting the income tax withholding or payment, if any, that may have been made for its distribution

MPI: Proportional amount of corporate income tax paid abroad referred to in the third paragraph of this article

MPI2: Proportional amount of corporate income tax paid abroad referred to in the fourth paragraph of this article

T: Rate referred to in Article 9 of this Law

ID: Tax creditable referred to in the first and sixth paragraphs of this article that corresponds to the dividend or profit received by the legal entity resident in Mexico

When the legal entity that in the terms of the preceding paragraphs has the right to credit the income tax paid abroad is spun off, the right to the credit will correspond exclusively to the spun-off company. When the latter disappears, it may transfer it to the spun-off companies in the proportion in which the capital stock is divided as a result of the spin-off.

In the case of individuals, the amount of the creditable tax referred to in the first paragraph of this article will not exceed the amount resulting from applying the provisions of Chapter XI of Title IV of this Law to the income received in the year from a source of wealth located abroad, once the deductions authorized for such income have been made in accordance with the corresponding chapter of the aforementioned Title IV. For these purposes, the deductions that are not exclusively attributable to the income from a source of wealth located abroad must be considered in the aforementioned proportion.

In the case of individuals who determine the tax corresponding to their income from business activities under the terms of Chapter II of Title IV of this Law, the amount of the creditable tax referred to in the first paragraph of this article will not exceed the amount resulting from applying to the total foreign income the rate established in article 152 of this Law. For these purposes, deductions that are not attributable exclusively to income from a source of wealth located abroad must be considered in the aforementioned proportion. For purposes of this paragraph and the preceding paragraph, the calculation of the crediting limits will be made for each country or territory in question.

Individuals residing in Mexico who are subject to the payment of tax abroad by virtue of their nationality or citizenship may make the credit referred to in this article up to an amount equivalent to the tax they would have paid abroad had they not had such status.

When the creditable tax is within the limits referred to in the preceding paragraphs and cannot be totally or partially credited, the credit may be made in the following ten fiscal years, until it is exhausted. For the purposes of this crediting, the provisions on losses of Chapter V of Title II of this Law will be applied, as applicable.

The part of the tax paid abroad that is not creditable in accordance with this article will not be deductible for purposes of this Law.

In order to determine the amount of the tax paid abroad that may be credited under the terms of the second and fourth paragraphs of this article, the respective exchange conversion must be made, considering the last exchange rate published in the Official Journal of the Federation, prior to the last day of the fiscal year to which the profit against which the dividend or profit received by the resident in Mexico is paid. In the other cases referred to in this article, for purposes of determining the amount of tax paid abroad that may be credited, the exchange conversion will be made considering the monthly average of the daily exchange rates published in the Official Gazette of the Federation in the calendar month in which the tax is paid abroad through withholding or remittance.

Taxpayers who have paid income tax abroad in an amount that exceeds the amount provided for in the treaty to avoid double taxation that, as the case may be, is applicable to the income in question, may only credit the excess in the terms of this article once the dispute resolution procedure contained in the same treaty has been exhausted.

No crediting of the tax paid abroad will be allowed when its withholding or payment is conditioned to its crediting under the terms of this Law.

Taxpayers must have proof of payment of the tax in all cases. In the case of taxes withheld in countries with which Mexico has entered into comprehensive information exchange agreements, a withholding certificate will suffice.

Entities resident in Mexico that obtain income from dividends or profits distributed by companies resident abroad, must calculate the proportional amounts of taxes and the limit referred to in paragraph seven of this article, for each fiscal year from which the distributed dividends originate. For purposes of the foregoing, legal entities resident in Mexico will be required to keep a record that allows identifying the fiscal year to which the dividends or profits distributed by the company resident abroad correspond. In the event that the legal entity resident in Mexico does not have elements to identify the fiscal year to which the dividends or profits distributed correspond, the record referred to in this paragraph will consider that the first profits generated by such company are the first to be distributed. Taxpayers must keep all the documentation that proves the information indicated in the record referred to in this paragraph. Mexican residents who do not keep the aforementioned record or documentation, or who do not perform the calculation in the manner indicated above, will not be entitled to credit the tax referred to in the second and fourth paragraphs of this article. The record mentioned in this paragraph must be kept as of the acquisition of the shareholding, but it must contain the information related to the profits in respect of which dividends or profits are distributed, even if they correspond to previous years.

When a resident abroad has a permanent establishment in Mexico and income from a source located abroad is attributable to such establishment, crediting may be made in accordance with the terms set forth in this article, only for that attributable income that has been subject to withholding.

A tax paid abroad will be considered to have the nature of an income tax when it complies with the provisions of the general rules issued by the Tax Administration Service. A tax paid abroad will be considered to be an income tax when it is expressly indicated as a tax included in a treaty to avoid double taxation in force to which Mexico is a party.

The crediting provided for in the first paragraph of this article will not be granted when the tax has also been credited in another country or jurisdiction for a reason other than a crediting similar to that indicated in the second and fourth paragraphs of this article, unless the income for which such tax was paid has also accrued in the other country or jurisdiction where the tax has been credited. The crediting provided for in the second and fourth paragraphs of this article will not be granted when the dividend or profit distributed represents a deduction or an equivalent reduction for the foreign resident entity that makes such payment or distribution.

Paragraph added DOF 09-12-2019

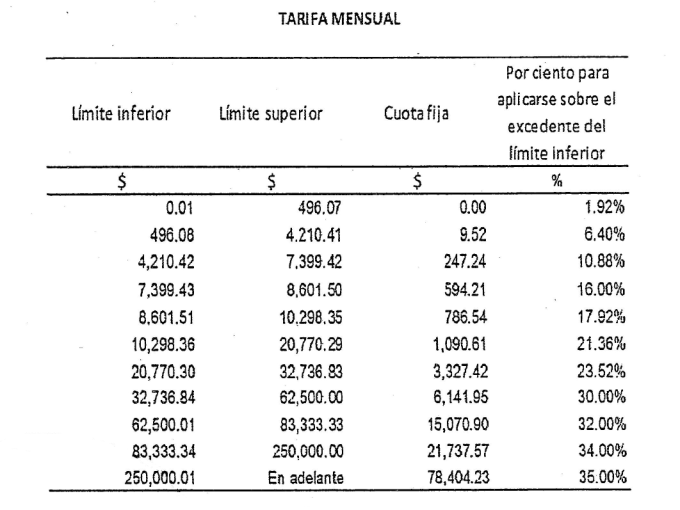

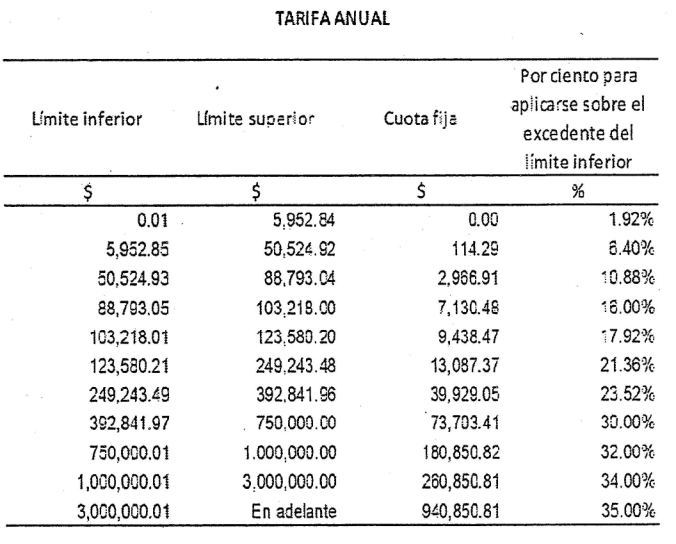

Article 6. When this Law provides for the adjustment or updating of the values of goods or transactions, which due to the passage of time and because of price changes in the country have varied, the following shall apply:

I. To calculate the modification in the value of the goods or operations in a period, the corresponding adjustment factor shall be used in accordance with the following:

a) When the period is one month, the monthly adjustment factor will be used, which will be obtained by subtracting the unit of the quotient resulting from dividing the National Consumer Price Index of the month in question by the aforementioned index of the immediately preceding month.

b) When the period is longer than one month, the adjustment factor will be obtained by subtracting the unit of the quotient resulting from dividing the National Consumer Price Index of the most recent month of the period by the index corresponding to the oldest month of such period.

II. To determine the value of a good or transaction at the end of a period, the restatement factor will be used, which will be obtained by dividing the National Consumer Price Index of the most recent month of the period, by the said index corresponding to the oldest month of said period.

When this Law refers to a legal entity, it is understood to include, among others, corporations, decentralized agencies that predominantly carry out business activities, credit institutions, civil societies and associations and joint ventures when they carry out business activities in Mexico.

In those cases in which reference is made to shares, it will be understood to include equity contribution certificates issued by national credit companies, partnership interests, participations in civil associations and ordinary participation certificates issued on the basis of share trusts that are authorized in accordance with the applicable legislation on foreign investment. When reference is made to shareholders, this will include the holders of the certificates referred to in this paragraph, of the partnership interests and of the participations mentioned above. In the case of companies whose capital is represented by shares, when reference is made in this Law to the proven cost of acquisition of shares, the proportional part represented by the shares in the capital stock of the company in question must be considered.

For the purposes of this Law, the financial system is comprised of Banco de México, credit, insurance and bonding institutions, financial group holding companies, general deposit warehouses, retirement fund administrators, financial leasing companies, credit unions, popular financial companies, variable income investment funds, debt instrument investment funds, financial factoring companies, brokerage firms and foreign exchange houses, whether resident in Mexico or abroad. Multiple purpose financial companies referred to in the General Law of Credit Organizations and Auxiliary Activities that have accounts and documents receivable derived from the activities that must constitute their main corporate purpose, in accordance with the provisions of such Law, that represent at least 70% of their total assets, or that have income derived from such activities and from the sale or administration of loans granted by them, that represent at least 70% of their total income, will be considered to be members of the financial system. For purposes of determining the 70% percentage, assets or income derived from the sale on credit of goods or services of the companies themselves, the sale of credit cards or financing granted by third parties will not be considered. The Tax Administration Service may issue the general rules necessary for the due and correct application of this paragraph.

Amended paragraph DOF 18-11-2015, 12-11-2021

In the case of newly created multiple purpose companies, the Tax Administration Service, by means of a particular resolution that considers the compliance program submitted by the taxpayer, may establish for the first three fiscal years of such companies, a percentage lower than that indicated in the preceding paragraph, in order to be considered as part of the financial system for the purposes of this Law.

For the purposes of this law, social welfare is considered to be the disbursements made to satisfy contingencies or present or future needs, as well as the granting of benefits in favor of workers or partners or members of cooperative societies, aimed at their physical, social, economic or cultural improvement, which allow them to improve their quality of life and that of their families. In no case shall be considered social welfare the expenditures made in favor of persons who do not have the character of workers or partners or members of cooperative societies.

For the purposes of this Law, securities depositories are considered to be credit institutions, investment fund operating companies, investment fund share distribution companies, brokerage firms and institutions for the deposit of securities in the country granted by the Federal Government in accordance with the provisions of the Securities Market Law, which provide securities custody and administration services.

Amended paragraph DOF 18-11-2015

For the purposes of this Law, interest, regardless of the name by which it is designated, is considered to be the yield of credits of any kind. It is understood that, among others, are interests: yields on public debt, bonds or debentures, including discounts, premiums and prizes; premiums on repurchase agreements or securities loans; the amount of commissions corresponding to the opening or guarantee of credits; the amount of the considerations corresponding to the acceptance of a guarantee, the granting of a guarantee or liability of any kind, except when such considerations must be made to insurance or bonding institutions; the gain on the sale of bonds, securities and other debt securities, provided that they are those that are placed among the general investing public, in accordance with the general rules issued for such purpose by the Tax Administration Service.

In financial factoring transactions, the gain derived from the credit rights acquired by financial factoring companies and multiple purpose financial companies will be considered as interest.

In financial leasing contracts, interest is considered to be the difference between the total payments and the original amount of the investment.

The assignment of rights over the income from granting the temporary use or enjoyment of real estate will be considered as a financing transaction; the amount obtained from the assignment will be treated as a loan, and the rents accrued under the contract must be accrued, even when these are collected by the acquirer of the rights. The consideration paid for the assignment will be treated as a credit or debt, as the case may be, and the difference with the rents will be treated as interest. The amount of the credit or debt will generate the annual adjustment for inflation under the terms of Chapter III of Title II of this Law, which will be cumulative or deductible, as the case may be, considering for its quantification, the discount rate taken for the assignment of the right, the total of the rents covered by the assignment, the value paid for such rents and the term determined in the contract, under the terms established in the Regulations of this Law.

When credits, debts, transactions or the amount of payments of financial leasing contracts are adjusted by applying indexes, factors or in any other way, including the use of investment units, the adjustment will be considered as part of the interest.

The treatment established by this Law for interest will be given to the exchange gains or losses accrued by the fluctuation of foreign currency, including those corresponding to the principal and interest itself. The exchange gain and loss may not be less than or exceed, respectively, that which would result from considering the exchange rate to settle obligations denominated in foreign currency payable in the Mexican Republic established by the Bank of Mexico, published for such purpose in the Official Gazette of the Federation, corresponding to the day on which the corresponding gain or loss is received or suffered.

Amended paragraph DOF 12-11-2021

The treatment established in this Law for interest will be given to the gain from the sale of the shares of the investment funds in debt instruments referred to in the Investment Funds Law.

Amended paragraph DOF 18-11-2015

TITLE II

OF LEGAL ENTITIES

GENERAL PROVISIONS

Article 9. Entities must calculate income tax by applying a 30% rate to the taxable income obtained in the fiscal year.

The taxable income for the year will be determined as follows:

I.The taxable income will be obtained by deducting from the total accumulated income obtained in the fiscal year, the deductions authorized by this Title and the employee profit sharing paid in the fiscal year, in the terms of Article 123 of the Political Constitution of the United Mexican States.

II.The taxable income for the year will be reduced, if applicable, by the tax loss carryforwards from previous years.

The tax for the fiscal year shall be paid by means of a tax return to be filed with the authorized offices within three months following the date on which the fiscal year ends.

In order to determine the taxable income referred to in paragraph e) of section IX of Article 123, paragraph A of the Political Constitution of the United Mexican States, workers' profit sharing paid in the year and tax losses pending application from previous years will not be reduced.

For the determination of the taxable income in the matter of employee profit sharing, taxpayers must deduct from the taxable income the amounts that would not have been deductible under the terms of section XXX of Article 28 of this Law.

Article 10. Entities that distribute dividends or profits must calculate and pay the tax corresponding to such dividends or profits, applying the rate established in Article 9 of this Law. For these purposes, the dividends or profits distributed will be added to the income tax payable under the terms of this article. In order to determine the tax to be added to the dividends or profits, these must be multiplied by the factor of 1.4286 and the rate established in Article 9 of this Law will be applied to the result. The tax corresponding to the distributed profits referred to in Article 78 of this Law will be calculated in accordance with the terms of said precept.

In the case of the distribution of dividends or profits through the increase of corporate shares or the delivery of shares of the same legal entity or when they are reinvested in the subscription and payment of the capital increase of the same person within 30 calendar days following their distribution, the dividend or profit will be deemed to have been received in the calendar year in which the reimbursement is paid due to the reduction of capital or liquidation of the legal entity in question, under the terms of Article 78 of this Law.

There is no obligation to pay the tax referred to in this article when the dividends or profits come from the net tax profit account established in this Law.

The tax referred to in this article shall be paid in addition to the tax for the year referred to in Article 9 of this Law, shall be considered a final payment and shall be paid to the authorized offices no later than the 17th day of the month immediately following the month in which the dividends or profits were paid.

When the taxpayers referred to in this article distribute dividends or profits and as a consequence thereof pay the tax established in this article, they may credit such tax in accordance with the following:

I. The crediting may only be made against the income tax of the year payable by the legal entity in the year in which the tax referred to in this article is paid.

The amount of the tax that cannot be credited in accordance with the preceding paragraph may be credited against the tax for the year and against the provisional payments of the same in the following two years. When the tax for the year is less than the amount that would have been credited in the provisional payments, only an amount equal to the latter will be considered creditable against the tax for the year.

When the taxpayer does not credit in a fiscal year the tax referred to in the fourth paragraph of this article, when it could have done so in accordance with the same, it will lose the right to do so in subsequent fiscal years up to the amount in which it could have done so.

II.For the purposes of Article 77 of this Law, in the year in which the tax is credited in accordance with the preceding section, taxpayers must reduce the net taxable income calculated in accordance with the terms of said provision, the amount resulting from dividing the tax credited by the factor 0.4286.

For the purposes of this article, dividends or distributed profits shall not be considered as distributed dividends or profits, the participation of workers in the profits of the companies.

Entities that distribute the dividends or profits referred to in Article 140 sections I and II of this Law, will calculate the tax on such dividends or profits by applying the rate established in Article 9 of this Law to such dividends or profits. This tax will be definitive.

In the case of interest derived from loans granted to corporations or permanent establishments in the country of residents abroad, by persons resident in Mexico or abroad, who are related parties of the person paying the loan, taxpayers will consider, for purposes of this Law, that the interest derived from such loans will have the tax treatment of dividends when any of the following events occur:

I. The debtor formulates in writing an unconditional promise of partial or total payment of the credit received, at a date determinable at any time by the creditor.

II. Interest is not deductible in accordance with the provisions of Section XIII of Article 27 of this Law.

III.In case of default by the debtor, the creditor has the right to intervene in the management or administration of the debtor company.

IV. The interest to be paid by the debtor is conditioned to the obtainment of profits or its amount is fixed based on such profits.

V. The interest derives from loans backed by credits, even when granted through a financial institution resident in the country or abroad.

For the purposes of this section, secured loans are considered to be transactions whereby a person provides cash, goods or services to another person, who in turn provides cash, goods or services directly or indirectly to the first mentioned person or to a related party of the first mentioned person. Also, transactions in which a person grants financing and the credit is secured by cash, cash deposits, shares or debt instruments of any kind, of a related party or of the borrower itself, to the extent that it is so secured, are also considered to be secured loans. For these purposes, it is considered that the loan is also secured under the terms of this section, when its granting is conditioned to the execution of one or several contracts that grant an option right in favor of the lender or a related party of the lender, the exercise of which depends on the partial or total nonpayment of the loan or its accessories by the borrower.

The set of financial transactions derived from debt or those referred to in Article 21 of this Law, entered into by two or more related parties with the same financial intermediary, where the transactions of one of the parties give rise to the others, with the primary purpose of transferring a defined amount of resources from one related party to the other, will be treated as backed credits as referred to in this section. This treatment will also apply to debt securities discount transactions that are settled in cash or in goods, which in any way fall under the circumstances described in the preceding paragraph.

Transactions in which financing is granted to a person and the loan is secured by shares or debt instruments of any kind owned by the borrower or by related parties of the borrower that are residents of Mexico, when the lender cannot legally dispose of them, will not be considered as secured loans, except in the case that the borrower fails to comply with any of the obligations agreed in the respective loan agreement.

Financing transactions other than those previously referred to in this article, which derive interest payable by legal entities or permanent establishments in the country of residents abroad, when such transactions lack a business reason, will also be treated as secured loans.

Paragraph added DOF 12-11-2021

Within the month following the date on which the liquidation of a company is completed, the liquidator must file the final tax return for the liquidation year. The liquidator must file monthly provisional payments on account of the tax for the liquidation year, no later than the 17th day of the month immediately following the month to which the payment corresponds, under the terms of Article 14 of this Law, until the total liquidation of the assets is carried out. The assets of establishments located abroad will not be considered in such provisional payments. At the end of each calendar year, the liquidator must file a tax return no later than January 17th of the following year, in which it will determine and pay the tax corresponding to the period from the beginning of the liquidation until the last month of the year in question and will credit the provisional and annual payments made previously corresponding to the aforementioned period. The last return will be for the year of liquidation, will include the assets of the establishments located abroad and must be filed no later than the month following the month in which the liquidation ends, even if twelve months have not elapsed since the last return.

For the purposes of this Law, it will be understood that a legal entity resident in Mexico is liquidated when it ceases to be a resident of Mexico under the terms of the Federal Tax Code or in accordance with the provisions of a treaty to avoid double taxation in force entered into by Mexico. For these purposes, all assets that the legal entity has in Mexico and abroad will be considered disposed of and their value will be considered to be the market value at the date of the change of residence; when such value is not known, the appraisal carried out for such purposes by the person authorized by the tax authorities will be used. The tax determined must be paid within 15 days following the date of the change of tax residence.

For the purposes of the preceding paragraph, a legal representative must be appointed who meets the requirements established in Article 174 of this Law. Such representative must keep at the disposal of the tax authorities the supporting documentation related to the payment of the tax on behalf of the taxpayer, during the term established in the Federal Tax Code, counted as of the day following the day in which the tax return was filed.

The legal representative appointed under the terms of this article will be jointly and severally liable for the taxes payable by the legal entity resident in Mexico that is being liquidated.

When business activities are carried out through a trust, the trustee shall determine under the terms of Title II of this Law, the tax result or loss of such activities in each fiscal year and shall comply on behalf of all the trustees with the obligations set forth in this Law, including the obligation to make provisional payments.

The trustee shall issue to the trustees or settlors, as the case may be, a tax receipt evidencing the income and withholdings derived from the business activities carried out through the trust in question.

The trustees will accrue to their other income for the year, the portion of the tax result of such year derived from the business activities carried out through the trust that corresponds to them, in accordance with the provisions of the trust agreement, and will credit in that proportion the amount of the provisional payments made by the trustee. The tax loss derived from the business activities carried out through the trust may only be reduced from the tax profits of subsequent years derived from the activities carried out through the same trust under the terms of Chapter V of Title II of this Law.

When there are tax losses pending to be reduced upon termination of the trust, the restated balance of such losses will be distributed among the trustees in the proportion corresponding to them according to the terms of the trust agreement and may be deducted in the year in which the trust is terminated up to the restated amount of their contributions to the trust not recovered by each of the trustees individually.

For the purposes of the preceding paragraph, the trustee shall maintain a capital contribution account for each of the trustees, in accordance with the provisions of Article 78 of this Law, in which the cash and property contributions made to the trust by each of them shall be recorded.

Deliveries of cash or property from the trust made by the trustee to the trustees will be considered repayments of contributed capital until such capital is recovered and will reduce the balance of each of the individual capital contribution accounts maintained by the trustee for each of the trustees until the balance of each such account is exhausted.

For purposes of determining the tax profit or loss for the year derived from the business activities carried out through the trust, the deductions will include that which corresponds to the assets contributed to the trust by the trustor when he/she is also the trustee and does not receive any consideration in cash or other assets for them, considering as acquisition cost thereof the original amount of the updated investment not yet deducted or the average cost per share, depending on the asset in question, that the settlor has at the time of its contribution to the trust, and that same acquisition cost must be recorded in the trust accounting and in the contribution capital account of the corresponding party. The settlor who contributes the assets referred to in this paragraph may not deduct such assets in the determination of its tax profits or losses derived from its other activities.

When the assets contributed to the trust referred to in the preceding paragraph are returned to the settlors who contributed them, they will be considered reintegrated at the tax value they have in the trust's accounting at the time they are returned, and at that same value they will be considered reacquired by the persons who contributed them.

The provisional income tax payments corresponding to the business activities carried out through the trust will be calculated in accordance with the provisions of Article 14 of this Law. In the first calendar year of operations of the trust or when no profit coefficient results in accordance with the above, the profit coefficient for the purposes of the provisional payments will be considered to be that which corresponds under the terms of Article 58 of the Federal Fiscal Code, to the preponderant activity carried out through the trust. For such purposes, the trustee will file a tax return for its own activities and another one for each of the trusts.

When any of the trustees is an individual resident in Mexico, he/she will consider as income from business activities the portion of the taxable income or profit derived from the business activities carried out through the trust that corresponds to him/her in accordance with the terms of the contract.

Foreign residents who are trustees are considered to have a permanent establishment in Mexico for the business activities carried out in Mexico through the trust and must file their annual income tax return for their share of the taxable income or profit for the year derived from such activities.

In cases where no trustees have been appointed or cannot be identified, it will be understood that the business activities carried out through the trust are carried out by the settlor.

The trustees or, as the case may be, the settlor, shall be liable for the breach of the obligations to be performed by the trustee on their behalf.

Article 14. Taxpayers shall make monthly provisional payments on account of the tax for the fiscal year, no later than the 17th day of the month immediately following the month to which the payment corresponds, in accordance with the bases indicated below:

I. The profit coefficient corresponding to the last twelve-month period for which a tax return was or should have been filed shall be calculated. For this purpose, the taxable income of the year for which the coefficient is calculated shall be divided by the nominal income of the same year.

Entities that distribute advances or income under the terms of Section II of Article 94 of this Law, will add to the taxable income or reduce the tax loss, as applicable, the amount of the advances and income, if any, distributed to their members under the terms of the aforementioned section, in the year for which the coefficient is calculated.

In the case of the second fiscal year, the first provisional payment will include the first, second and third month of the fiscal year, and the tax profit ratio of the first fiscal year will be considered, even if it has not been twelve months.

When in the last twelve-month fiscal year there is no profit ratio in accordance with the provisions of this section, the profit ratio corresponding to the last twelve-month fiscal year for which such ratio exists shall be applied, provided that such fiscal year is not more than five years prior to the year for which the provisional payments must be made.

II. The tax profit for the provisional payment will be determined by multiplying the profit coefficient that corresponds in accordance with the previous section, by the nominal income corresponding to the period from the beginning of the fiscal year until the last day of the month to which the payment refers and, if applicable, the following concepts will be deducted:

a) The amount of employee profit sharing paid in the same fiscal year, under the terms of Article 123 of the Political Constitution of the United Mexican States. The aforementioned amount of employee profit sharing must be reduced, in equal parts, in the provisional payments corresponding to the months of May through December of the fiscal year. The decrease referred to in this paragraph will be made in the provisional payments of the fiscal year in a cumulative manner and the amount that is decreased in terms of this paragraph will in no case be deductible from the taxpayer's cumulative income, in accordance with the provisions of Section XXVI of Article 28 of this Law.

For the purposes of the preceding paragraph, the reduction of employee profit sharing shall be made up to the amount of the tax profit determined for the corresponding provisional payment and in no case shall the profit coefficient determined under the terms of section I of this article be recalculated.

b) The legal entities that distribute advances or yields in the terms of section II of Article 94 of this Law, will reduce the tax profit with the amount of the advances and yields that they distribute to their members in the terms of the mentioned section, in the period from the beginning of the fiscal year and up to the last day of the month to which the payment refers. A tax receipt must be issued stating the amount of the advances and yields distributed, as well as the tax withheld.

c) The tax loss from prior years pending application against taxable income, without prejudice to the reduction of such loss against taxable income for the year.

Reformed fraction DOF 09-12-2019

III. The provisional payments will be the amounts resulting from applying the rate established in Article 9 of this Law, on the taxable income determined under the terms of the preceding section, and the provisional payments of the same period made previously may be credited against the tax payable. The withholding made to the taxpayer during the period may also be credited against such provisional payments, under the terms of Article 54 of this Law.

In the case of the liquidation period, in order to calculate the corresponding monthly provisional payments, the profit coefficient for the purposes of such provisional payments will be considered to be that which corresponds to the last return that at the end of each calendar year the liquidator had filed or should have filed under the terms of Article 12 of this Law or that which corresponds in accordance with the provisions of the last paragraph of Section I of this Article.

The nominal income referred to in this article will be the cumulative income, except for the annual cumulative inflation adjustment. In the case of loans or transactions denominated in investment units, interest as accrued, including the corresponding adjustment to the principal because the loans or transactions are denominated in such units, will be considered nominal income for the purposes of this article.

Taxpayers that initiate operations as a result of a merger of companies in which a new company arises, will make provisional payments in such year as of the month in which the merger occurs. For the purposes of the foregoing, the profit ratio referred to in the first paragraph of Section I of this Article will be calculated considering jointly the profits or tax losses and the income of the merging companies. In the event that the merging companies are in their first fiscal year of operation, the coefficient will be calculated using the items indicated corresponding to said fiscal year. When there is no coefficient in the terms of this paragraph, the provisions of the last paragraph of section I of this article will be applied, considering the provisions of this paragraph.

Taxpayers that initiate operations as a result of the spin-off of companies will make provisional payments as of the month in which the spin-off occurs, considering, for that year, the profit coefficient of the spin-off company in that year. The coefficient referred to in this paragraph will also be used for the purposes of the last paragraph of Section I of this Article. The spin-off company will consider as provisional payments effectively paid prior to the spin-off, the totality of such payments made in the fiscal year in which the spin-off occurred and they cannot be assigned to the spun-off companies, even when the spin-off company disappears.

Taxpayers must file the provisional payment returns whenever there is tax payable, credit balance or when it is the first return in which there is no tax payable. Taxpayers must not file provisional payment returns in the year of initiation of operations, when they have filed the notice of suspension of activities provided for in the Regulations of the Federal Tax Code or in cases where there is no tax payable or credit balance and it is not the first return with this characteristic.

In order to determine the provisional payments referred to in this article, taxpayers shall be subject to the following:

a) Income from a source of wealth located abroad that has been subject to income tax withholding and income attributable to its establishments located abroad that are subject to income tax in the country where these establishments are located will not be considered.

b) Taxpayers who consider that the profit coefficient to be applied to determine provisional payments is higher than the profit coefficient of the year to which such payments correspond may, as from the second half of the year, request authorization to apply a lower coefficient. When as a result of the authorization it appears that the provisional payments have been paid in a lower amount than the amount that would have corresponded to them, surcharges will be paid for the difference between the payments made applying the lower coefficient and those that would have corresponded to them if such coefficient had not been applied, by means of the respective supplementary return.

Subsection amended DOF 12-11-2021

Article 15. Taxpayers subject to a reorganization proceeding may reduce the amount of the debts forgiven in accordance with the agreement entered into with their recognized creditors, under the terms established in the Bankruptcy Law, from the losses pending reduction that they have in the fiscal year in which said creditors forgive the aforementioned debts. When the amount of the forgiven debts is greater than the tax loss carryforwards, the resulting difference will not be considered as taxable income, unless the forgiven debt arises from transactions between and with related parties referred to in Article 179 of this Law.

CHAPTER I

OF INCOME

Article 16. Entities resident in Mexico, including joint ventures, will accrue all income in cash, goods, services, credit or of any other type, obtained during the year, including income from their establishments abroad. The annual cumulative inflation adjustment is the income obtained by taxpayers from the real decrease in their debts.

For the purposes of this Title, income obtained by the taxpayer from capital increases, payment of losses by its shareholders, premiums obtained from the placement of shares issued by the company itself or from using the equity method to value its shares, as well as income obtained from the revaluation of its assets and capital are not considered income for purposes of this Title.

Income from economic or monetary support received by taxpayers through programs provided for in the federal or state budgets are not considered taxable income for purposes of this Title, provided that the programs have a list of beneficiaries; the resources are distributed through electronic transfer of funds in the name of the beneficiaries; the beneficiaries comply with the obligations established in the rules of operation of such programs, and have a favorable opinion from the competent authority regarding compliance with tax obligations, when they are obliged to request it under the terms of the tax provisions. The expenses or disbursements made with the economic support referred to in this paragraph, which are not considered accruable income, will not be deductible for purposes of this tax. The federal or state agencies or entities in charge of granting or administering the economic or monetary support, must make available to the general public and keep updated in their respective electronic media, the list of beneficiaries referred to in this paragraph, which must contain the following data: corporate name of the beneficiary legal entities, the amount, resource, benefit or support granted for each one of them and the territorial unit.

Paragraph added DOF 30-11-2016

Other income that will not be considered accruable for purposes of this Title, are the considerations in kind in favor of the contractor referred to in articles 6, section B and 12, section II of the Income Law on Hydrocarbons, provided that for the determination of the income tax payable by the contractor, the value of the mentioned considerations when these are disposed of or transferred to a third party is not considered as deductible cost of goods sold in the terms of article 25, section II of this Law. The income obtained from the sale of the goods received as consideration will be accruable under the terms established in this Law.

Paragraph added DOF 30-11-2016

Entities residing abroad, as well as any entity that is considered a legal entity for tax purposes in its country, that have one or more permanent establishments in the country, will accrue the total income attributable to such permanent establishments. The simple remittance obtained from the head office of the legal entity or from another establishment of the legal entity will not be considered as income attributable to a permanent establishment.

For taxpayers under this Title, income from dividends or profits received from other legal entities resident in Mexico will not be taxable.

For the purposes of Article 16 of this Law, it is considered that income is obtained, in those cases not provided for in other articles of this Law, on the dates indicated in accordance with the following in the case of:

I. Sale of goods or rendering of services, when any of the following events occurs, whichever occurs first:

a) The tax receipt is issued to cover the price or consideration agreed upon.

b) The good is materially shipped or delivered or when the service is rendered.

c) The total or partial price or consideration agreed upon is collected or payable, even if it comes from advances.

In the case of income from the rendering of independent personal services obtained by corporations or civil associations and income from the supply of potable water for domestic use or domestic garbage collection services obtained by decentralized agencies, concessionaires, permit holders or companies authorized to provide such services, it is considered that such income is obtained at the time the agreed price or consideration is collected.

II. Granting of the temporary use or enjoyment of goods, when all or part of the consideration is collected, or when such consideration is payable to the person making the grant, or when the tax receipt is issued to cover the price or consideration agreed upon, whichever occurs first.

III. Obtaining income from financial leasing contracts, taxpayers may choose to consider as income obtained in the year the total of the agreed price or the portion of the price payable during the year.

In the case of forward sales under the terms of the Federal Tax Code, taxpayers will consider as income obtained in the year the total of the agreed price.

The option referred to in the first paragraph of this section must be exercised for all the contracts. The option may be changed without requirements only once; in the case of the second and subsequent changes, at least five years must elapse from the last change; when the change is intended to be made before such period elapses, the requirements established for such purpose in the Regulations of this Law must be complied with.

When in terms of the first paragraph of this section, the taxpayer has opted to consider as income obtained in the year only the portion of the agreed price payable and sells the documents pending collection, or gives them in payment, it must consider the amount pending accrual as income obtained in the year in which the sale or payment is made.

In the event of noncompliance with financial lease contracts, in respect of which the option has been exercised to consider as income obtained in the year only the portion of the price payable, the lessor will consider as income obtained in the year, the amounts payable in the year from the lessee, reduced by the amounts that have already been returned in accordance with the respective contract.

In the case of financial leasing contracts, income derived from any of the options referred to in Article 15 of the Federal Tax Code will be considered income obtained in the year in which they become due.

IV. Income derived from debts not covered by the taxpayer, in the month in which the statute of limitations period expires or in the month in which the period referred to in the second paragraph of section XV of Article 27 of this Law expires.

Taxpayers that enter into real estate construction contracts will consider the income from such contracts as accruable on the date on which the estimates for work performed are authorized or approved for collection, provided that the payment of such estimates takes place within the three months following their approval or authorization; otherwise, the income from such contracts will be considered accruable until they are actually paid. Taxpayers that enter into other work contracts in which they are obligated to execute said work in accordance with a plan, design and budget, will be considered to obtain the income on the date on which the estimates for work executed are authorized or approved so that they may be collected, provided that the payment of said estimates takes place within the three months following their approval or authorization; Otherwise, the income from such contracts will be considered accruable until they are effectively paid, or in cases where they are not required to present them or the periodicity of their presentation is greater than three months, the quarterly progress in the execution or manufacture of the goods referred to in the work will be considered accruable income. The accruable income from work contracts referred to in this paragraph will be reduced by the portion of the advances, deposits, guarantees or payments for any other concept, which had been previously accrued and which is amortized against the estimate or progress.

The taxpayers referred to in the preceding paragraph will consider as accumulable income, in addition to those indicated therein, any payment received in cash, goods or services, whether in the form of advances, deposits or guarantees for the fulfillment of any obligation, or any other.

For the purposes of this Title, the following are considered accruable income, in addition to those indicated in other articles of this Law:

I. The income determined, including presumptively by the tax authorities, in the cases in which it is applicable according to the tax laws.

II. The gain derived from the transfer of ownership of property by payment in kind. In this case, in order to determine the gain, the value of the property in question on the date on which its ownership is transferred by payment in kind will be considered as income, according to the appraisal performed by a person authorized by the tax authorities, and the deductions allowed by this Law for the case of disposal may be reduced from such income, provided that the requirements established therein and in the other tax provisions are complied with. In the case of merchandise, as well as raw materials, semi-finished or finished products, the total income will be accrued and the value of the cost of what is sold will be determined in accordance with the provisions of Section III, Chapter II, Title II of this Law.

III. Those coming from constructions, installations or permanent improvements in real estate, which in accordance with the contracts by which their use or enjoyment was granted, are for the benefit of the owner. For these purposes, the income is considered to be obtained at the end of the contract and in the amount that at that date the investments have according to the appraisal made by a person authorized by the tax authorities.

IV. The gain derived from the sale of fixed assets and land, securities, stocks, shares, partnership interests or equity contribution certificates issued by national credit companies, as well as the realized gain derived from the merger or spin-off of companies and the gain derived from the reduction of capital or liquidation of commercial companies residing abroad, in which the taxpayer is a partner or shareholder.

In cases of capital reduction or liquidation of corporations resident abroad, the gain will be determined in accordance with the provisions of Section V of Article 142 of this Law.

In the case of mergers or spin-offs of companies, the gain derived from such acts will not be considered cumulative income when the requirements established in Article 14-B of the Federal Tax Code are met.

V. Payments received for recovery of a loan deducted for uncollectible.

VI. The amount recovered from insurance, bonds or third party liabilities, in the case of losses of the taxpayer's property.

VII. The amounts that the taxpayer obtains as indemnification to compensate him for the decrease in his productivity caused by the death, accident or illness of technicians or managers.

VIII. The amounts received to incur expenses on behalf of third parties, unless such expenses are supported by tax receipts in the name of the party on whose behalf the expense is incurred.

IX. Interest accrued in favor during the fiscal year, without any adjustment. In the case of delinquent interest, as of the fourth month, only the interest actually collected will be accrued. For these purposes, income from late payment interest received after the third month following the month in which the debtor is in default is considered to cover, in the first instance, the late payment interest accrued in the three months following the month in which the debtor is in default, until the amount received exceeds the amount of accrued late payment interest accrued for the last mentioned period.

For the purposes of the preceding paragraph, delinquent interest charged will accrue until such time as the interest actually charged exceeds the amount of delinquent interest accrued in the first three months and up to the amount by which it exceeds the amount of delinquent interest.

X. The annual adjustment for inflation that is accruable under the terms of Article 44 of this Law.