Home / Mexican Government / Executive Power / Finance Ministry / SAT in Mexico

SAT in Mexico is something you will probably come to hate if you decide to start a business in Mexico. Understanding the Servicio de Administración Tributaria (SAT) is not merely a financial compliance task. Moreover, SAT, Mexico’s federal tax authority, is one of the most sophisticated, data-driven, and deeply integrated tax agencies in the world. Accordingly, its influence extends far beyond collecting taxes, touching every aspect of daily business operations, from issuing an invoice and processing payroll to moving goods across the country.

To the uninitiated, SAT’s reputation can be formidable. However, viewing it as a mere obstacle is a strategic misstep. Instead, it is the central nervous system of Mexico’s formal economy—a powerful institution that ensures a level playing field, enforces fiscal discipline, and provides a framework of operational transparency. Its advanced digital ecosystem, while demanding, ultimately reduces corruption and provides a degree of certainty unparalleled in many other jurisdictions.

Firstly, we designed this guide for foreign executives, investors, and operational managers, we certainly hope you find value in it. Secondly, this guide will demystify SAT in Mexico, moving beyond technical jargon to provide a clear, overview of its functions, core components, and the critical obligations your business will face. Thirdly, We will cover the foundational pillars of your company’s fiscal identity—the RFC, the e.firma, and the CSD—and provide an in-depth analysis of the revolutionary CFDI e-invoicing system. By the end of this article, you will not only understand the requirements for compliance but will also appreciate how a proactive and informed approach to SAT in Mexico is a key enabler of long-term success in the Mexican market overall.

Servicio de Administración Tributaria

Tax Administration Service

The Tax Administration Service (SAT) is a decentralized administrative body of the Ministry of Finance and Public Credit (SHCP). It is the highest tax authority responsible for collecting taxes in Mexico.

| Year Founded | 1997 |

|---|---|

|

Chief |

|

|

Dependant Of |

Ministry of Finance and Public Credit (SHCP) |

|

Dependencies |

Registro Federal de Contribuyentes (RFC) |

The Servicio de Administración Tributaria, or SAT, is the autonomous federal agency responsible for administering and enforcing tax and customs law in Mexico. While it is often compared to the Internal Revenue Service (IRS) in the United States or HMRC in the United Kingdom, this comparison only tells part of the story. SAT operates under the direction of Mexico’s Ministry of Finance and Public Credit (Secretaría de Hacienda y Crédito Público – SHCP), but its operational scope and real-time integration into business activities are far more extensive than its counterparts in many other G20 nations.

What truly sets SAT apart is its pioneering adoption of technology altogether. So, over the past two decades, Mexico has systematically built a digital-first tax administration framework. Hence, SAT in Mexico gains unprecedented, real-time visibility into the economic activities of the entire country with this system. As a result, for a business, this means that compliance is not a once-a-year event but a constant, daily process embedded in your core operational software. Basically, understanding this digital reality is the first step to mastering your obligations.

Before your Mexican company can earn a single peso of revenue or hire an employee, it must establish its unique fiscal identity with SAT in Mexico. Three critical, non-negotiable digital assets comprised this identity altogether.

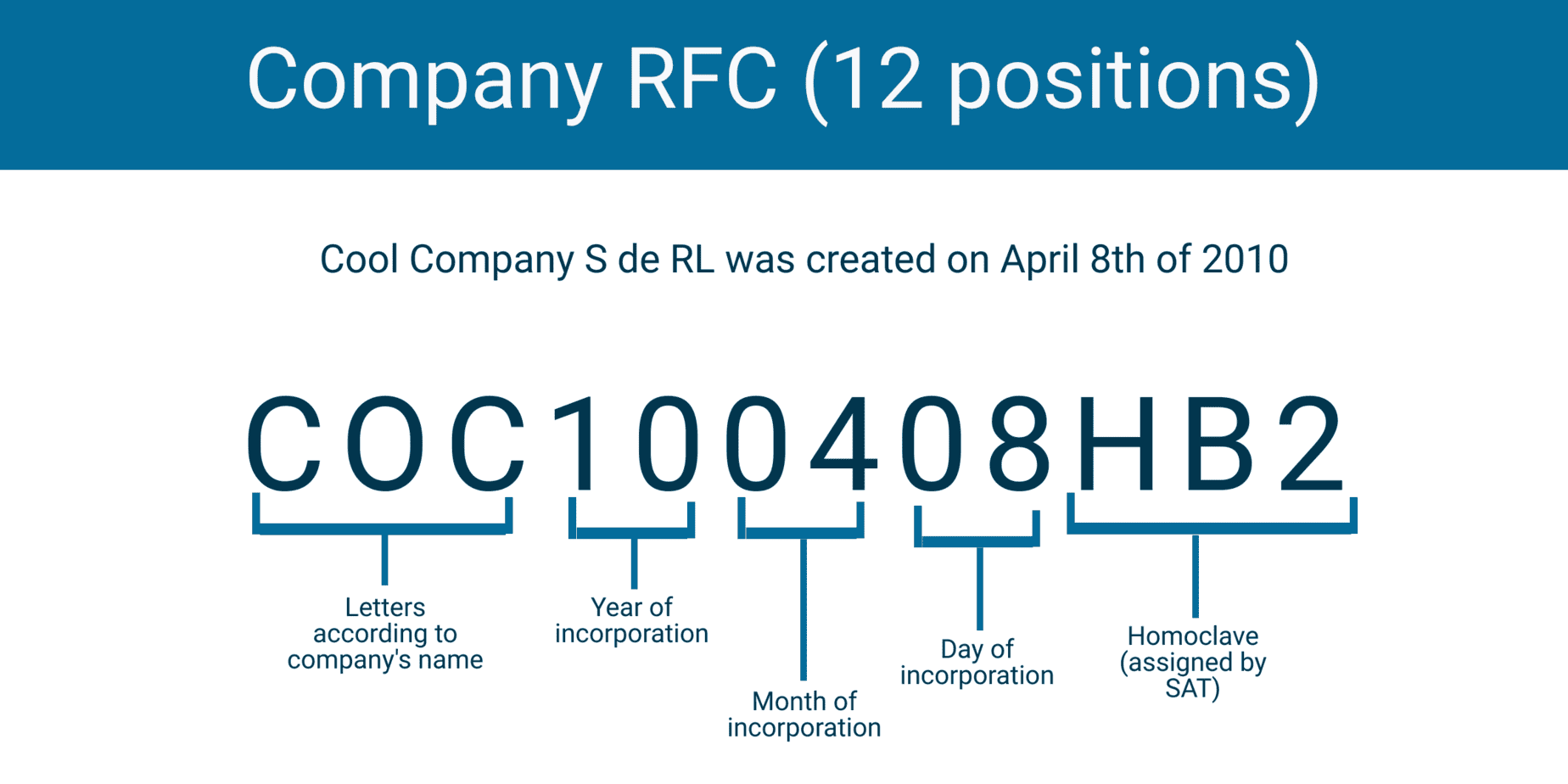

The RFC is the single most important identifier your company will possess in Mexico. It is basically a unique alphanumeric code. SAT assigns one to every individual and legal entity that it requires to pay taxes.

If the RFC is your company’s fingerprint, the e.firma is its legally binding signature. Formerly known as the FIEL (Firma Electrónica Avanzada), the e.firma is a set of encrypted digital files that legally identifies the user in the digital realm. It holds the same legal weight as a handwritten signature.

.cer), a private key file (.key), and a password created by the user. The private key is known only to the user, ensuring that only they can generate a valid digital signature.While the e.firma is used to authenticate the company itself, the Digital Seal Certificate (CSD) is used for a more specific, high-volume task: digitally “sealing” or signing every single electronic invoice (CFDI) the company issues.

Understanding the CFDI is the single most important step in understanding day-to-day operations in Mexico. The CFDI, or “Online Digital Tax Receipt,” is the cornerstone of SAT’s digital ecosystem. It is far more than just an invoice; it is the sole, legally recognized proof of any commercial transaction.

The Mexican system mandates that every invoice be digitally certified by SAT in near real-time before it can be considered legally valid. This process creates a transparent, unbreakable chain of data between a business, its customers, and the tax authority. Here is how it functions.

This entire process, known as timbrado (stamping), typically takes less than two seconds. The strategic implication is profound: SAT in Mexico has a complete record of your company’s revenue at the very moment you bill your client.

The CFDI framework extends to virtually every type of commercial document, creating a unified digital language for business transactions. Key types include:

Operating within this ecosystem has major strategic consequences:

While the CFDI system is the how, the core taxes are the what. A Mexican corporation is primarily responsible for two major federal taxes.

ISR is the corporate income tax levied on the profits of your company. The Mexican Income Tax Law regulates the specifics of this tax.

IVA is a consumption tax. SAT applies it to nearly all sales of goods, services, and leases. For businesses, it functions as a pass-through tax. The Mexican VAT Law regulates the specifics of this tax.

Navigating SAT in Mexico successfully requires diligent communication and impeccable compliance.

The Buzón Tributario (Tax Mailbox) is the official, secure electronic portal through which SAT in Mexico communicates with taxpayers. All official notifications, audit requests, information requirements, and resolutions are delivered through this mailbox. By law, taxpayers are required to keep their mailbox activated and check it regularly. An email notification is sent when a new message arrives, but failure to see the email is not a valid excuse for missing a legal deadline. Ignoring the Buzón Tributario is one of the most serious compliance errors a company can make.

The Mexican Servicio de Administración Tributaria has engineered a tax administration system that is demanding, comprehensive, and technologically advanced. For foreign businesses, it requires a significant upfront investment in understanding its processes and a permanent commitment to operational discipline.

However, to view this system merely as a burden is to miss the larger strategic picture. The radical transparency enforced by the CFDI ecosystem creates a remarkably level playing field, reducing the “informal” or “grey” economy and ensuring that all competitors are held to the same fiscal standards. It provides the Mexican state with the fiscal certainty to fund infrastructure and social programs, contributing to long-term national stability. For your business, it means that your legally compliant operations are protected from fraudulent practices by suppliers or customers.

Successfully navigating SAT in Mexico is a foundational element of risk management and operational excellence. It requires the right systems, the right processes, and, most importantly, the right local expertise. A partner that understands the nuances of the CFDI, the intricacies of tax declarations, and the proper way to manage communications with the authority is indispensable. By embracing the discipline that SAT demands, your company can build a resilient, transparent, and highly successful operation, fully integrated into the vibrant heartbeat of one of the world’s most critical economies.

Starting operations in Mexico?